Market Commentary - June 2025

“Those who were seen dancing were thought to be insane by those who could not hear the music.”

— Philosopher Friedrich Nietzsche

Tap Dance or Tango?

Tap dance is an individual form of dance while the tango requires close partnership and movements together. It has been a year of delicate footwork for the markets, as market participants have been dealing with the pronouncement and retraction of tariffs. The ebbs and flows of tariff negotiations have driven the good and bad days in the markets for much of the year. Even before the announcements, the markets were holding their breath to see what things would look like. On April 2 (Liberation Day), President Trump announced his long-promised “reciprocal” tariffs — declaring a ten percent baseline tax on imports from all countries and higher rates for dozens of nations that run trade surpluses with the U.S. The S&P 500 dropped nearly 12% in the following three business days. Announcements of pauses on the tariffs have generally been received well by the markets and have led Wall Street pundits to call it the “TACO” trade or Trump Always Chickens Out.

It's Raining Tacos!

In late May, Trump postponed the 50% tariffs he had announced just days earlier. Further, the U.S. Court of International Trade (CIT) added to the optimism by ruling that many existing tariffs were improperly enacted, only for an appeals court to reverse the mood later that day by pausing the decision. Then, just a few days later, Trump accused China of violating an informal agreement about reciprocal tariffs. Clearly markets are moving based on tariffs, trade, and reciprocity. Further, even if the CIT ruling is affirmed, there are many mechanisms for the U.S. to reinstate some level of new tariffs.

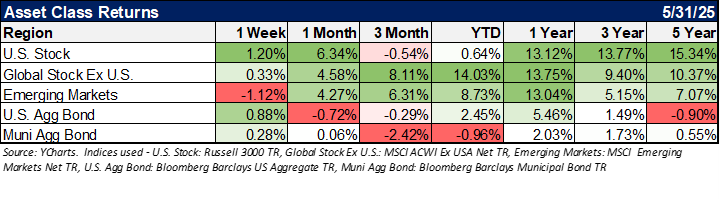

“Sell in May and go away” proved to be bad advice this year. According to Yardeni research, since 1928 the S&P 500 has been flat for May. This year the S&P 500 returned +6.2%, marking its biggest monthly advance since November 2023. There is a great deal of uncertainty for the markets at any given time, but right now the range of outcomes seems extremely wide. While the tariffs and trade protectionism have added to the volatility this year-to-date, they have not significantly decreased stock market levels, as most of the major indices are positive for the year.

Let us not forget about bonds here as well. On May 16th, Moody’s downgraded the U.S. debt rating from Aaa to Aa1. This has not yet been a problem, but the yield curve has changed shape since the beginning of the year. The intermediate levels in the curve have come down significantly, anticipating Fed Rate changes and a slowing economy. The long end of the curve is telling us that financing the U.S. government debt will be more expensive in the future. I would not call this great news:

So Where Do We Stand?

You would think that there is some glaring weakness in portfolios with all the headlines in the first five months of the year, but global equities are positive, taxable bonds are positive, and alternatives (specifically Gold) are also positive. There are pockets of weakness in Municipals, Small Cap Stocks, and certain stock sectors, but a well-balanced portfolio has held up very well through May. We believe there is certainly more volatility to come given the ever-evolving tariff story, fiscal spending battles in Congress, monetary policy decisions, and all the other “known unknowns.” So, it is important to buckle up for a potentially bumpy ride.

As always, don’t hesitate to contact us to discuss your tolerance for risk and whether your portfolio is in alignment with your goals.

From the Investments Desk at MDL Wealth Management and Journey Strategic Wealth

This material is distributed for informational purposes only. Investment Advisory services offered through MDL Wealth Management, a DBA of Journey Strategic Wealth, LLC, a registered investment adviser registered with the U.S. Securities and Exchange Commission ("SEC"). The views expressed are for informational purposes only and do not take into account any individual’s personal, financial, or tax considerations. Opinions expressed are subject to change without notice and are not intended as investment advice. Past performance is no guarantee of future results. Please see Journey Strategic Wealth’s Form ADV Part 2A and Form CRS for additional information.

Securities offered through Purshe Kaplan Sterling Investments, Member FINRA/SIPC, Headquartered at 80 State Street, Albany NY 12207. Purshe Kaplan Sterling Investments and Journey Strategic Wealth d/b/a MDL Wealth Management are not affiliated companies. Not FDIC Insured. Not Bank Guaranteed. May lose value including loss of principal. Not insured by any state or federal agency.